BizChina

- Details

- By Daniel Gross

- Hits: 1734

For nearly 150 years, American businesspeople have been entranced by the possibilities of China—an unimaginably huge, virgin market. If only the Middle Kingdom were to develop into a thriving consumer society, it would be an incredible playground for American brands and companies—bigger and more profitable, potentially, than the U.S. domestic market. (See Thomas McCormick’s The China Market for an excellent history of this idea.) It hasn't quite worked out. Revolutions, communism, state control of the economy, enduring poverty and the tendency of the Chinese to save rather than spend have all proven to be formidable obstacles.

The Chinese operations of many American companies are still dwarfed by their massive domestic operations. Wal-Mart, for example, had 246 stores in China as of March 31, serving just 7 million Chinese customers weekly—a tiny portion of the population. But now, thanks to macroeconomic upheaval in the U.S. and China, the promise of the China market finally seems to be within reach. Exports to China are up about 25 percent in the first quarter of 2009 from 2008, but they're still tiny, just $5.5 billion in March. More significant has been the rapid growth of U.S.-branded products that are made and marketed in China.

Exhibit A: The Wall Street Journal reported today that Citigroup made far more money in China last year than it did in the U.S. That's not saying much, since Citi notched a $27.68 billion loss in 2008, mostly from its U.S. operations. But as James Areddy reports, the bank's "net income in China jumped 95 percent in 2008 to the equivalent of $191 million, helped by a 20 percent rise in commercial foreign-exchange transactions."

Exhibit B. General Motors. In April, GM sold 173,007 vehicles in the U.S., down 34 percent from April 2008. The same month, GM's China sales jumped 25 percent to a record 151,084. It's always dangerous simply to forecast by extrapolation, but the trends are undeniable. If GM's monthly China sales increase 7 percent from current levels and the carmaker's U.S. monthly sales decrease by 7 percent from current levels, then GM—more accurately, GM and its joint-venture partners—will be selling more cars in China than in GM's home country.

Exhibit C: YUM Brands, the parent of Pizza Hut, KFC, Taco Bell and Long John Silver's. Last year, YUM's restaurant count in the U.S. was basically unchanged. But its China unit, which comprises mainland China, Thailand and KFC Taiwan, opened 500 new restaurants and tallied operating profits of $469 million. With 2,980 restaurants and a new outlet opening almost every day, Yum Brands says KFC is the "largest and fastest growing restaurant chain in mainland China today." In the U.S., by contrast, the number of KFCs has fallen each of the last four years, from 5,525 in 2004 to 5,253 in 2008. Sales data show that KFC's U.S. operations still outsell its Chinese operations, by a margin of $5.2 billion to $3.6 billion. But when you back out sales of franchisees, the stores owned by YUM brands in China sold $2.5 billion worth of greasy chicken goodness in 2008, compared with $1.2 billion for company-owned stores in the U.S.

For the near term, it looks as if these trends will continue, and not just because the U.S. market for banking, cars and fast food is mature and shrinking while the Chinese markets for those goods and services is immature and growing. We may also be witnessing some fundamental shifts in trans-Pacific consumer behavior. As Geoff Dyer writes in an excellent Financial Times article, China's savings rate was a stunning 50 percent of GDP in 2007. But the Chinese consumer is more cautious than cheap. "Many Chinese put a large chunk of their wages into bank accounts because they are worried about pensions, education expenses and—most of all—the prospect of a big hospital bill if a family member falls seriously ill," Dyer writes. Ironically, the same may be said of post-credit-boom Americans, who are socking away cash instead of buying stuff made in China. Thanks to the global slump, The New York Times noted, Chinese exports overall were off 22.6 percent in April. And in the first quarter of 2009, according to the Commerce Department, Chinese exports to the U.S. fell 10.8 percent from the 2008 first quarter.

To make up for lost exports and to keep all those factories humming, China's government is now focusing on ways to bolster domestic consumer spending. A key form of stimulus, Dyer writes, will be boosting the government's role in providing health care. China has an ambitious effort underway to build clinics and has pledged to cover 90 percent of the population with some form of health insurance by 2011. More than tax cuts or public works spending, the thinking goes, a stronger safety net could spur Chinese consumers to spend less and save more.

In other words, the fact that China's population may soon be insulated from some of the ill health effects of eating KFC and driving Buicks might free up more cash for middle-class workers in Shenzhen to eat more KFC and buy more Buicks.

- Details

- By Chinaview.cn

- Hits: 1824

China is advancing its study of plans to allow foreign companies to list on the Shanghai Stock Exchange and may work out preliminary arrangements as early as this year, industry sources said yesterday.

The country is expected to step up communications with other nations in the coming months on the development of an international board in the city after concluding a deal with Britain on Monday for further stock-market reform, the sources said.

"China agrees to allow qualified foreign companies, including United Kingdom companies, to list on its stock exchange through issuing shares or depository receipts in accordance with relevant prudential regulations," the two countries said in a joint statement issued on Monday.

The agreement, reached by Chinese Vice Premier Wang Qishan and British Finance Minister Alistair Darling following a meeting in London, is set to pave the way for large British companies like HSBC to sell shares in Shanghai.

HSBC said in a statement yesterday that it "would like to be the first foreign bank to list in Shanghai if the authorities allow," and is working toward that goal. It did not give a specific timetable for a stock sale in the city.

Peter Wong, executive director of HSBC subsidiary Hongkong & Shanghai Banking Corp, said earlier this month that a Shanghai listing would consolidate HSBC's brand influence and raise funds for expansion in the Chinese mainland market.

Two years ago, China started to consider permitting foreign companies to issue yuan shares to help boost the status of its fledgling stock market on the mainland. But the program has proceeded slowly as regulators worked to ease investor jitters over a stock glut.

Program revived

Read more: Plans moving forward to enable foreign firms to list in Shanghai

- Details

- By David Cao

- Hits: 1670

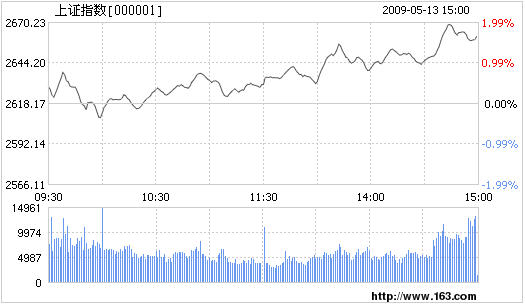

Chinese shares rose 1.74 percent Wednesday as investors' confidence got a boost from April retail sales figures, which analysts said indicated that government stimulus efforts were having a positive impact.

The benchmark Shanghai Composite Index rose 1.74 percent, or 45.59 points, to close at 2,663.77. The Shenzhen Component Index edged up 1.13 percent, or 115.22 points, to 10,294.37.

Gains outnumbered losses by 514 to 315 in Shanghai and 475 to 242 in Shenzhen.

Combined turnover climbed to 222.89 billion yuan (32.63 billion U.S. dollars) from 176.3 billion yuan on Tuesday.

Retail sales rose 14.8 percent in April year on year to 934.32 billion yuan, the National Bureau of Statistics (NBS) announced Wednesday.

The growth rate was 0.1 percentage point higher than in March.

Industry support plans for the machinery and nonferrous metal sectors, released on Tuesday and Monday respectively, were also helping maintain economic growth, the analysts said.

- Details

- By Chinadaily.com.cn

- Hits: 1872

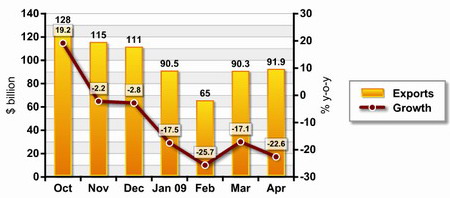

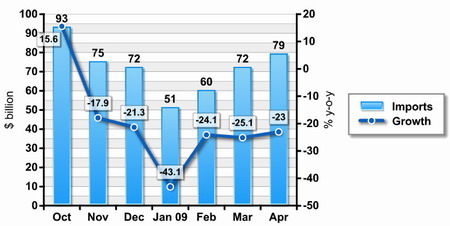

China's exports and imports shrank for the sixth month in row in April, the General Administration of Customs said on Tuesday.

Exports fell 22.6 percent in April from the same period a year ago to $91.94 billion. Imports were down 23 percent to $78.8 billion.

The trade surplus was $13.14 billion.

A CITIC Securities analyst said the weakening global economic outlook, depreciation of major Asian currencies, as well as the resurgence of protectionism continued to impede China's exports. It is likely to continue throughout the first half of the year, said the analyst.

The combined foreign trade in April was worth $170.73 billion, down 22.8 percent year on year, but that was up 10.4 percent from that for March.

Exports in the four months to April totaled $337.42 billion, down 20.5 percent, and imports went down 28.7 percent to $261.99 billion over the same period.

- Details

- By Chinaview.cn

- Hits: 1605

PetroChina and PDVSA, the national oil company of Venezuela, have established a joint venture on oil exploration and development, said Jiang Jiemin, Chairman of PetroChina Company Limited here Tuesday.

PetroChina held 40 percent of the new company's shares, Jiang told Xinhua at the annual shareholders meeting.

According to Jiang, a joint venture transporting oil and two joint refineries would also be established. PetroChina would hold 50 percent stake in the former and 60 percent in the latter two.

One of the refineries would be located in eastern Guangzhou Province, Jiang said.

PetroChina is expected to produce 40 million tons of crude oil from Venezuela annually, Jiang said.

He also noted that construction of the China part of the pipeline transmitting crude oil from Russia to China will be started this month and the transmission capacity is expected to expand from the current annual 15 million tons.

Taking advantages of the decreased prices of oil and gas, PetroChina would expand its overseas business, and strengthen cooperation with both energy producers and international energy giants such as ExxonMobile, BP and Shell, Jiang said.

PetroChina is the Hong Kong and Shanghai-listed subsidiary of China National Petroleum Corporation, China's largest oil producer.

More Articles …

Page 120 of 126